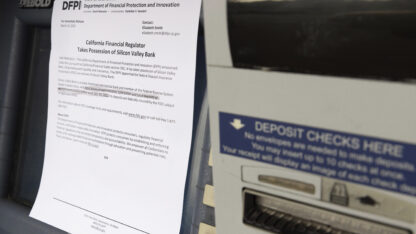

The sudden collapse of California-based Silicon Valley Bank sent depositors into panic and global markets into chaos as the U.S. government scrambled to prevent the fire from spreading to other banks, and possibly setting aflame the global banking system.

Silicon Valley Bank, or SVB, had been the 16th largest U.S. bank with more than $200 billion in assets and about $175 billion in deposits before it failed last Friday.

After SVB’s collapse, another bank, New York-based Signature Bank, followed. The Biden administration then announced it was taking extreme emergency measures to prevent a total crisis.

Read this story now for free

To continue reading, sign up for our newsletter and get unlimited access to WABE.org

You can select your preferences for news and local content. We will never share your email address. Learn how your newsletter sign-up will support WABE and Public Media